The culture of electronic media and the internet and the culture of social interaction continue to erode classical music and chamber music concert attendance. In the U.S., possibly some of this erosion is augmented by the economic downturn, but the trend has been relentlessly underway for many years now. Lifestyle and arts consumption choices of shifting generations continue to thwart traditional concert attendance, despite the fact that there are today more high-quality concert events and more diverse programming than ever before.

How long can this go on? Which organizations are likely to survive? How much does size (assets; revenue; financial strength) insure sustainability? Are there norms that are embodied by the strongest and best of the current contenders in this nonprofit chamber music marketplace, that other organizations in the field ought to aim for? Do the treasury management decisions of such leading organizations constitute norms that others should emulate? As weaker organizations begin to fail, will we see some of them get aggregated by joint-ventures or M&A into other larger ‘survivor’ organizations in the same geographic vicinity? And, if so, what are the financial ratios that potential acquirers should look for in due-diligence?

These are questions that are not readily answerable. But it does seem that tough, Darwinian survival-of-the-fittest times are ahead.

Just as you would do if you were evaluating companies and stocks, it’s helpful to consider the competitive landscape for chamber music ensembles by applying some financial-ratio analysis, to characterize the field quantitatively and monitor the players and the outcomes.

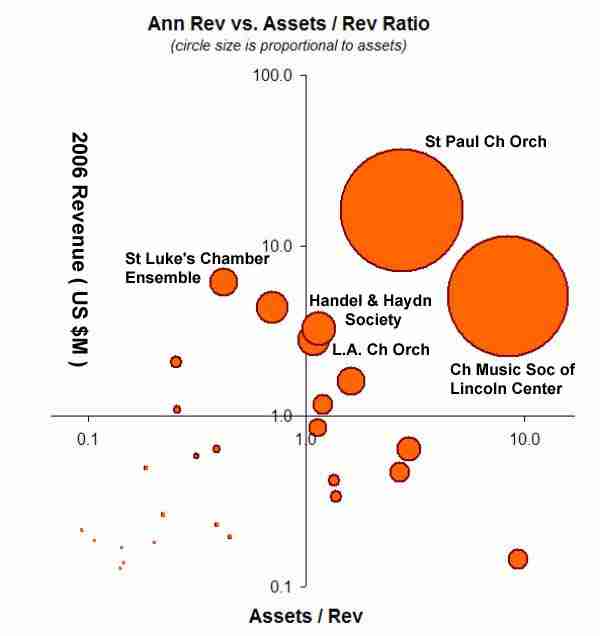

The log-log plot of the revenue vs. assets-to-revenue ratio shown above is for 35 nonprofit standing chamber orchestra organizations in the U.S. for the most recent year for which data are available, 2006. It provides at-a-glance comparison of top-line revenue and capital-output efficiency. I extracted the data from the federal IRS Form 990 tax documents that are publicly available via Guidestar and other sources. It’s easy to do—took me less than one hour. You may like to do this for your own organization, or for organizations that you make contributions to, to see how they are doing amongst their peers.

The upper-right quadrant contains ensembles that are both highly productive (in terms of revenue generation and free cashflow) and well-endowed. The upper-left quadrant contains ensembles that are very active but are relatively under-capitalized. The lower-right quadrant contains ensembles that are relatively well-endowed but are perhaps under-utilizing their available assets. And the lower-left quadrant contains organizations that are financially at-risk. Although this plot is strictly for standing chamber orchestras, the same sort of statistical distribution and scatter-plot could be done for 501(c)(3) chamber music presenter organizations and other groups. Robert Higgins’s and Richard Bull’s and Murray Dropkin’s books (links below) are particularly good, with regard to understanding and acting upon financial-ratio analysis for nonprofit organizations.

Possibly the most promising strategy for selling to the evolving chamber music market—of all ages—is social networking and Web 2.0 apps. Besides those environments, there are email affinity-marketing services, such as Emma.com, which are significantly more effective and flexible than services that were available several years ago.

When being chased by a bear, your survival first requires that you are not the slowest runner in the woods and that you are running in the best direction for getting away. I seriously doubt that the Federal Reserve will come to the rescue of any chamber music organizations ...

In this regard, the concept of sustainable growth was originally developed by Robert Higgins, Professor of Finance at the School of Business Administration, University of Washington. The sustainable growth rate (SGR) of any enterprise is the maximum rate of growth in sales that can be achieved, given the enterprise’s profitability, asset utilization, and debt (financial leverage) ratios. The variables in the SGR equation are the following:

- the net profit margin on new and existing revenues (P);

- the asset turnover ratio, which is the ratio of sales revenues to total assets (A);

- the retention rate, which is defined as the fraction of earnings retained in the business (R);

- the assets to beginning-of-period equity ratio (T).

The SGR increases when the operating margin increases, the assets to beginning-of-period equity increases, the asset turnover increases, or the retention rate increases. The sustainable growth model assumes that the firm wants to: (a) maintain a target capital structure without issuing new equity; and (b) increase sales as rapidly as market conditions allow.

Since the orchestras we are discussing are not-for-profits, the profit-margin term is a bit tricky. But the net income in the operating fund is a suitable proxy for what profit-margin would be in a for-profit enterprise, so the SGR equation can in fact be used for nonprofits.

The concept of sustainable growth can be helpful for planning healthy nonprofit growth. This concept forces managers to consider the financial consequences of sales increases and to set sales growth goals that are consistent with the operating and financial policies of the enterprise. Often, a conflict can arise if growth objectives are not consistent with the value of the organization's sustainable growth. If an orchestra’s sales expand at a rate that exceeds the sustainable rate, one or some combination of the four ratios must change. If an orchestra’s actual revenue growth rate temporarily exceeds the SGR, the required cash can usually be borrowed, against the orchestra’s line-of-credit. When actual growth exceeds the SGR for longer periods, management must formulate a financial strategy from among the following options: (1) permanently increase financial leverage (the issuance of debt); or (2) decrease the total assets to sales ratio. In practice, orchestras may be reluctant to undertake these steps. Orchestras are reluctant to issue debt because of high issue costs, and the unreliable nature of debt funding on terms favorable to the issuer. An orchestra can increase financial leverage only if it has unused debt capacity with assets that can be pledged and its debt-to-fund equity ratio is reasonable in relation to other nonprofits. Orchestras can attempt to liquidate marginal programs or intellectual property (such as trademarked broadcast programs or record labels, or branded educational/outreach content), increase ticket prices, or enhance production efficiencies to improve the financial ratios.

In summary, it is possible for an orchestra to grow too aggressively and rapidly, resulting in reduced liquidity and the need to deplete assets. Shrinking attendance and ticket sales is a worse problem, but it is not the only problem that can happen.

- Boulian P, Coppock B, Kinzey, Limbacher J, Tamburri L. Revenue Model. Conf of League of American Orchestras, 23-JUN-2007. [1MB pdf]

- ArtsJournal TheArtfulManager blog

- DSM. Niches and Long-Tailed Culture. CMT blog, 21-OCT-2006.

- DSM. SMS and Viral Chamber Music. CMT blog, 31-OCT-2006.

- Blazek J. Nonprofit Financial Planning Made Easy. Wiley, 2008.

- Brown D, Hayes N. Influencer Marketing: Who Really Influences Your Customers? Butterworths, 2008.

- Bull R. Financial Ratios: How to Use Financial Ratios to Maximise Value and Success for Your Business. CIMA, 2007.

- Dropkin M, Halpin J, LaTouche B. The Budget-Building Book for Nonprofits: A Step-by-Step Guide for Managers and Boards. Jossey-Bass, 2007.

- Dropkin M, Hayden A. The Cash Flow Management Book for Nonprofits: A Step-by-Step Guide for Managers and Boards. Jossey-Bass, 2007.

- Feuerhelm-Watts R. Wide Open: Inspiration & Techniques for Art Journaling on the Edge. Northlight, 2007.

- Gillin P. The New Influencers: A Marketer's Guide to the New Social Media. Quill Driver, 2007.

- Higgins R. Analysis for Financial Management. 7e. McGraw-Hill, 2004.

- Horowitz J. Classical Music in America. Norton, 2007.

- Horowitz J. Classical Music in America: A History of Its Rise and Fall. Norton, 2005.

- Maddox D. Budgeting for Not-for-Profit Organizations. Wiley, 1999.

- Smith, Bucklin & Associates. The Complete Guide to Nonprofit Management. Wiley, 1994.

- Walsh C. Key Management Ratios: The Clearest Guide to the Critical Numbers That Drive Your Business. FT/Prentice-Hall, 2005.

- Weber L. Marketing to the Social Web: How Digital Customer Communities Build Your Business. Wiley, 2007.

No comments:

Post a Comment